1031 Structure

General Information

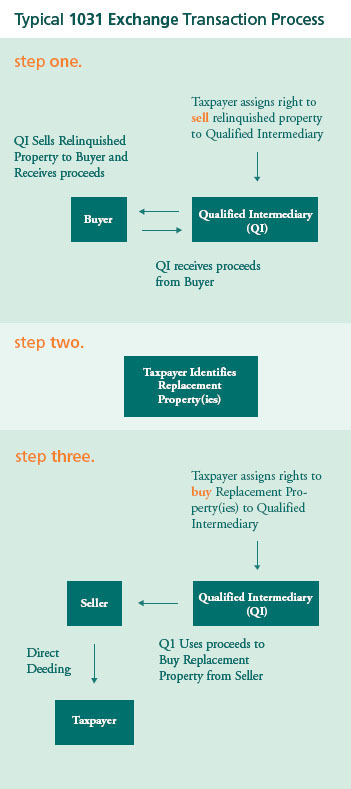

An IRC 1031 tax deferred exchange is a cost saving way to sell a rental or investment property and acquire another, without paying state (almost all states) and federal capital gains taxes. Once an IRC 1031tax deferred exchange is successfully completed, recognition of capital gains on the Relinquished Property is deferred.

The deferral of capital gains can continue through numerous exchanges and can even be eradicated upon the death of the Taxpayer.

Time Requirements

45 Day Requirement: From the date the Relinquished Property is disposed of, you have 45 days to identify your Replacement Properties.

180 Day Requirement: From the date the Relinquished Property is disposed of, you must complete the acquisition of the Replacement Property within the lesser of 180 days or the due date of the income tax return (including filed extensions for the year in which the relinquished property was exposed).

Related Party Issues

IRC Section 1031(f) states that in the event an exchange occurs between related parties then each party must not dispose of the property received in the exchange for a period of two years. In the event either party is disposed of prior to two years then the gain previously deferred is currently taxable (the “Two Year Rule”).

Since the Two Year Rule was codified, the IRS has continued to limit the viability of exchanges between related parties. If you are considering a related party exchange, you should proceed with extreme caution only after a careful review by counsel.

Partnership Issues

IRC Section 1031(a)(2)(D) prohibits tax deferral on an exchange of partnership interests. However, it is certainly possible for a partnership to exchange the real estate owned by the partnership for other “like kind” real estate in a tax deferred exchange.